Monday, October 9, 2023

What lessons do we learn from Nigeria’s financial markets since general election results were announced in March? What has happened to fixed income and equity markets? And where are they headed now?

FX

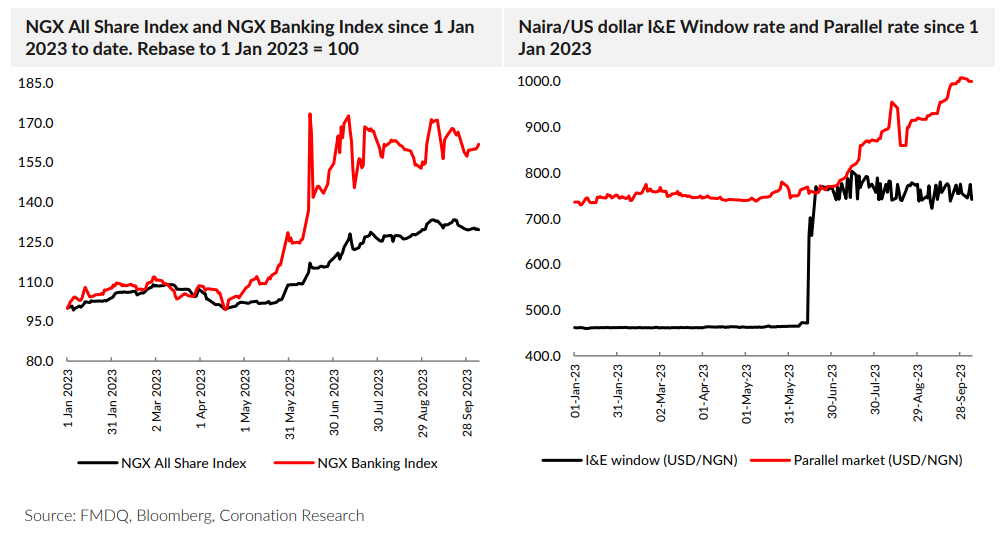

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 1.81% to close at ₦741.85/US$1. Similarly, at the parallel market, the Naira gained by 0.80% to close at ₦1,000.00/US$1. Currently, the gap between the I&E Window and the parallel market stands at 34.80%. Gross foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) slipped by 0.05% to US$33.22bn.

The divergence between the official and parallel market continues to widen due to pressures from the backlog of FX demand. This situation highlights the challenges of sustaining the policy though it is unclear what alternative policy could be adopted. It is likely a question of simultaneously tackling part of the backlog with specific measures while waiting for the problem to solve itself as demand for FX is satisfied in the parallel market. This will take some time, in our view, with little chance of a quick fix.

BONDS & T-BILLS

In the secondary market for treasury bills, performance was largely bullish as average yields declined by 45bps to 7.49% pa (versus 7.94% last week). Average yields fell at the short-end to 3.19% (-45 basis points), medium-end to 5.96% (-60 basis points) and at the long end of the yield curve to 10.13% (-36 basis points).

In case you missed it: All change in global markets

In the secondary market for FGN bonds, average yield also fell, in this case by 3bps to 14.41%. Average yields at the short end of the curve declined by 15 basis points to 12.37%; the mid-end remained unchanged at 14.74%, while at the long end, the average yield rose by 3 basis points to 15.62%.

From the FGN bond calendar for the fourth quarter of 2023 which was released last week, we deduce that the borrowing levels for the Federal Government is still quite elevated. Based on this, we may likely see rates go up further, although marginally. Movements in Naira bond yields have been quite small this year, as they were in 2022. We await announcements from the new management of the CBN as to any significant change in interest rate policy.

OIL

Last week, oil prices lost 11.26% to settle at US$84.58/bbl. Year-to-date, the price of Brent crude is down by 1.55% and it has been trading at an average of US$82.10/bbl year-to-date which is 17.15% lower than the average of US$99.09/bbl in 2022.

Last week’s decline was driven by concerns that consistently high interest rates may hinder global development and negatively affect demand. In the US Labour Department statistics reported that non-farm jobs increased by 336,000 in September, significantly above economists’ predictions of a 170,000 increase. While this was positive data for

current US growth it also suggested that US interest rates will be held high for a long time in 2024, which is negative for growth prospects. These demand-side factors outweighed the good news on the supply side, namely that Saudi Arabia and Russia have announced that they will keep their productions cuts until the end of the year.

Over the weekend war broke out between the Palestinian enclave of Gaza and Israel, bringing the prospect of renewed US sanctions on Iran and the risk of further conflict in the Middle East. This propelled Brent crude prices US$5.00/bbl upwards on Monday.

We maintain our view that, for most of the year, prices are likely to remain above the US$75.00/bbl mark set in Nigeria’s government budget.

EQUITIES

Last week, the NGX All-Share Index rebounded by 0.11% to settle at 66,454.57 points. Its year-to-date return rose to 29.66%. Oando (+14.65%), BUA Cement (+9.94%), and Airtel Africa (+8.53%) closed positive while Dangote Cement (-8.79%), Cadbury Nigeria (-6.83%), and Nigerian Breweries (-5.75%) closed negative. Performances across the NGX

sub-indices were mostly positive as the NGX Banking Index (+1.43%) topped the list, followed by, NGX Pension (+0.81%), NGX Consumer Goods (+0.17%) and NGX-30 (+0.07%) indices closing green. The NGX Oil and Gas closed flat (+0.00%) while the NGX Insurance (-3.11%) and NGX Industrial Goods (-1.38%) indices closed in the red.

Market trends six months after the election

Six months on from the announcement of President Bola Ahmed Tinubu’s victory in presidential elections, what is the state of Nigeria’s financial markets and where are they headed? It is helpful to re-read what we published at the beginning of March. The All Progressives Congress (APC) manifesto, which we took as a roadmap for future policy, gave readers little warning of the radical reform agenda the President would soon unleash. The manifesto was about, to paraphrase it quickly: going for economic expansion; achieving 10.0% per annum GDP growth; increasing government expenditure. So, we favoured Dangote Cement as a key stock to invest in the growth theme, food manufacturers, and the bank sector.

Then came the welcome news of a radical reform agenda, the first big announcement coming during the President’s inaugural address at the end of May. This was the ending of fuel subsidies (note that this was included in the APC

manifesto: few people thought it would actually happen). It was time for us to change our investment tactics. We wrote in Investment Opportunities from Fuel Subsidy Removal, June 9, that the benefits were clear for Federal Government of Nigeria Eurobonds (the FGN would have more US dollars with which to service them) and for mid-stream petroleum companies (thanks to unregulated margins): but the situation was worrying for the consumer (rising inflation) and therefore food manufacturers and brewers.

Soon came the announcement liberalising foreign exchange markets and the partial free-market float of Naira/US dollar exchange transactions. For us, the consequences were clear, as we expressed in Investment Opportunities from FX Liberalisation, July 10, namely that the listed banks were prime beneficiaries. The beauty of listed equity markets is the ability to switch between stocks quickly. Our initial preference (in March) for Dangote Cement did not do too badly (up 18.8% year-to-date and up 11.6% since the beginning of March), but the banking sector did much better (up 61.9% year-to-date, up 44.8% since the beginning of March, and up 11.3% since mid-July)

At the same time, these two key reforms have not run their course. There are still separate Importers & Exporters window and parallel market foreign exchange rates, and fuel subsidies seem to continue to some degree. Does this mean that the reform agenda has stalled and that we must revise our judgments again?

We think not. What has happened, in our view, is that these two key reforms have encountered more problems than initially envisaged, but they are not being abandoned. The backlog of demand of US dollars may not have been fully understood at the time the new policy was implemented. The rise in petroleum prices, initially from ₦184.0/litre to

₦488.0/litre (in Lagos), was exacerbated by the rise in the price of crude (Brent crude rose from US$72.7/bbl at the end

of May to US$84.6/bbl at the end of last week), rising to ₦620.3/litre (in Lagos, on average) in August. At the end of last week we saw prices in Lagos around the ₦578/litre mark while unregulated diesel traded at ₦980/litre.

The government is not back-tracking on its reforms. Measures to soften the impact of reforms are being rolled out, but the basic policy stance has not altered (despite many pleas for a change in policy).

The only area in which we still wait for direction is Naira interest policy, which for fixed income investors is a large part of the jigsaw that is still missing. Note that, just as in 2022, fixed income rates have changed only slightly so far this year, moving slightly upwards.

Why do we not have an interest rate policy in place? This is largely due to the lengthy process of appointing a new Governor of the Central Bank of Nigeria, who only took office a few weeks ago. The Governor does not inherit an easy

hand to play, far from it. The decision whether to pursue an interest rate policy designed to rein in inflation (and, if so, how aggressively to raise market interest rates), or whether to continue with market interest rates well below the rate of inflation (as they have been since the fourth quarter of 2019), is not an easy one. Fixed income investors with liquid assets would undoubtedly favour raising rates: the problem would be the effect on the cost of borrowing and its effect on the economy.

Looking Forward

Therefore, the investment outlook for Naira fixed income investments (T-bill, FGN bonds) remains unclear. Yields are well below the rate of inflation and investors are not rewarded very much for taking duration (i.e., buying long-dated FGN bonds as opposed to short-dated ones). Even deposit rates (which can be arranged by asset management companies on behalf of clients) are reasonably attractive for investors that have a short-term investment horizon when compared with T-bill and bond rates. And a good reason to have a short-term investment horizon is that rates may go up.

While rates remain below the level of inflation, risk is still in fashion. Equities are still performing well (although we think most of the heavy lifting of the NGX Exchange All-Share Index has been done already this year) and risk products still get investors’ attention. What investors need to understand is that they may need to change tactics again this year. Keep your options open.

Model Equity Portfolio

Last week the Model Equity Portfolio lost 0.01% compared with a rise in the NGX All-Share Index of 0.11%, underperforming it by 12bps. Year-to-date it has risen by 33.54% compared with a rise of 29.66% in the NGX All-Share

Index, outperforming it by 388bps.

Last week, we continued to make sales of our notional positions in banks, as advised in the last edition of the Nigeria Weekly Update. Then we looked at the performance of the banks in our Model Equity Portfolio and decided to take

stock. Our decision to makes banks overweight, back in June, was responsible for outperformance of 294 basis points

since then, which is the bulk of our outperformance year-to-date. By contrast, our decision to wind down that

overweight position and make a small underweight in banks, which we took towards the end of August, has cost us 6

basis points. We might just as well have hung on.

This is the advantage of having a performance attribution model. We can see what works and what does not.

Performance attribution does not tell us what to do in future, but it tells us how powerful or otherwise our decisions have been, and we can use it for sensitivity analysis. We intend to continue with a small underweight in banks but will assess, at the end of this week, what to do next and report back next Monday.

This week, we will continue to build up our notional position in Seplat Energy to a double overweight (we still have not

finished what we started three weeks ago, thanks to liquidity constraints). We notice that MTN Nigeria appears to be badly sold off and, from a tactical point of view, we intend to take a one percentage point overweight notional position in it this week. We plan no further changes this week.

Click here to download the full report.

Disclosure and Disclaimer

The analysts and Head of Research have prepared the report independently, using publicly available information. The information is believed to be accurate but not independently verified. The report is intended for the use of clients and should not be considered as a solicitation to buy or sell securities.

No liability is accepted for errors or omissions, and readers should conduct their own evaluations and consult with financial advisers before making investment decisions.

This report is not intended for individual investors and should not be distributed where prohibited by law or regulations.

Related Posts

Headed for higher rates?

The impact of the CBN’s directive to banks to sell down part of their net long US dollar positions seemed Read more

How big was the January equity rally?

How big was the rally in the NGX All-Share Index in January? The correct answer is 35.8%, but there is Read more

Airtel Africa and the Naira/US$ rate

What is driving the price of Airtel Africa and what does this say about the parallel exchange rate?

Evaluating the January rally and potential selling strategies

If you make money out of a January rally, should you hang on for the full year, or should you Read more