Many people assume that a family business is the most fragile form of investment. They believe it may not go further than two or three generations. For this reason, they might not want any involvement with it. According to Harvard Business Review, many articles or speeches about family businesses today include a reference to the three-generation rule. Conversations around this subject showed that most family-run businesses don’t survive beyond the three generations which re-echoes the Brazilian saying, rich father; noble son; poor grandson.

Ultimately, Harvard Business Review in the article then revealed that, “on average, data suggests family businesses last far longer than typical companies do. They dominate many of the longest lasting companies in the world.” This would be true of such family businesses as Antinori, William Clark & Sons, Guinness and a host of all other long-standing businesses.

Why not a family business?

With these businesses as proof, why then do people question the longevity of family-run businesses? Similarly, why do people still frown at the idea of starting a family-run business; given the fair amount of evidence showing that family-run businesses have survived many generations and economic meltdown? Or one can ask: what did successful family businesses do differently? How were they able to survive and dominate their industries for over a hundred years?

While we may not have answers to these questions, it is safe to conclude that family businesses that have been able to survive and thrive through all the hard times must have done some things differently. However, we all know that most companies will not disclose the secret of their success to others.

In this piece, however, we will highlight three major ways to beat the effects of an economic meltdown on your family-run business. With these steps serving as a guide to ensuring the success of your business combined with other factors peculiar to it, the longevity of your company will be greatly improved.

1. Define your goals

This is very crucial to the growth, success and longevity of your business. From the very start, define the goals for the company with specific timelines. Make your vision and mission bold, clear and understood by every employee. With that, employees will key into the goals of the company and be driven as well as motivated to work towards the achievement of such goals. In addition, the importance of teamwork by employees cannot be over-emphasized. All employees should see themselves as one family and co-owners of the company. With that, the survival of the company can be assured.

What would defining the goals of a new or already existing business look like? This would entail creating a strategic business plan that suits your kind of business. A financial plan should also be drawn up and followed. These plans should clearly outline the mission, vision and objectives of the business. It is important to note that it takes a consistent effort, with loyal and dedicated employees, to grow a successful business.

2. Create a budget

No matter how small the business is, there should be a budget for every expense. That way, the company’s money will not be spent rashly on items not provided for in the budget. It is natural to want everything, but it is smart to start with things that are relevant and most profitable.

The worst mistakes are made as a result of poor decision making but with a budget in place, that is strictly followed, some of these mistakes which could lead to the collapse of the business, could be avoided.

READ ALSO: Money and Social Climbing: The 4 Strategies You Don’t know that Will Set You Apart

3. Don’t forget the crisis management template!

Crisis, either man-made or natural, is bound to occur during the life span of a business. Therefore, it is wise to prepare for and make adequate provision on how to forestall or handle a crisis before it occurs. Many businesses have gone under after being hit by a crisis that was too severe for the business to recover from. A good example is the sudden departure of a CEO. Nothing should be taken for granted or ignored; there should be plans on how to replace key management staff if at any point in time, they cease to be available, and ultimately, a well-structured business succession plan.

A crisis management plan helps to identify potential problems in several categories/levels. The plan should highlight how to respond to and effectively manage any crisis that occurs. Proven damage control measures should be applied as soon as such negative risk happens, to minimize loss.

Are you considering starting or growing a family business? The right financial advisor can improve your chances of success and help you achieve your goals by providing you with tailor-made trade solutions.

Learn how a cross-border finance trading tool from Coronation Merchant Bank can empower your business with cutting-edge solutions in a convenient and simple way customized to suit the busy lifestyle of an entrepreneur.

Related Posts

What Happens When Income Stops? Retirement Planning Redefined

For most people, income feels predictable.It comes in regularly. It supports everything, from daily expenses to long-term plans. Over time, Read more

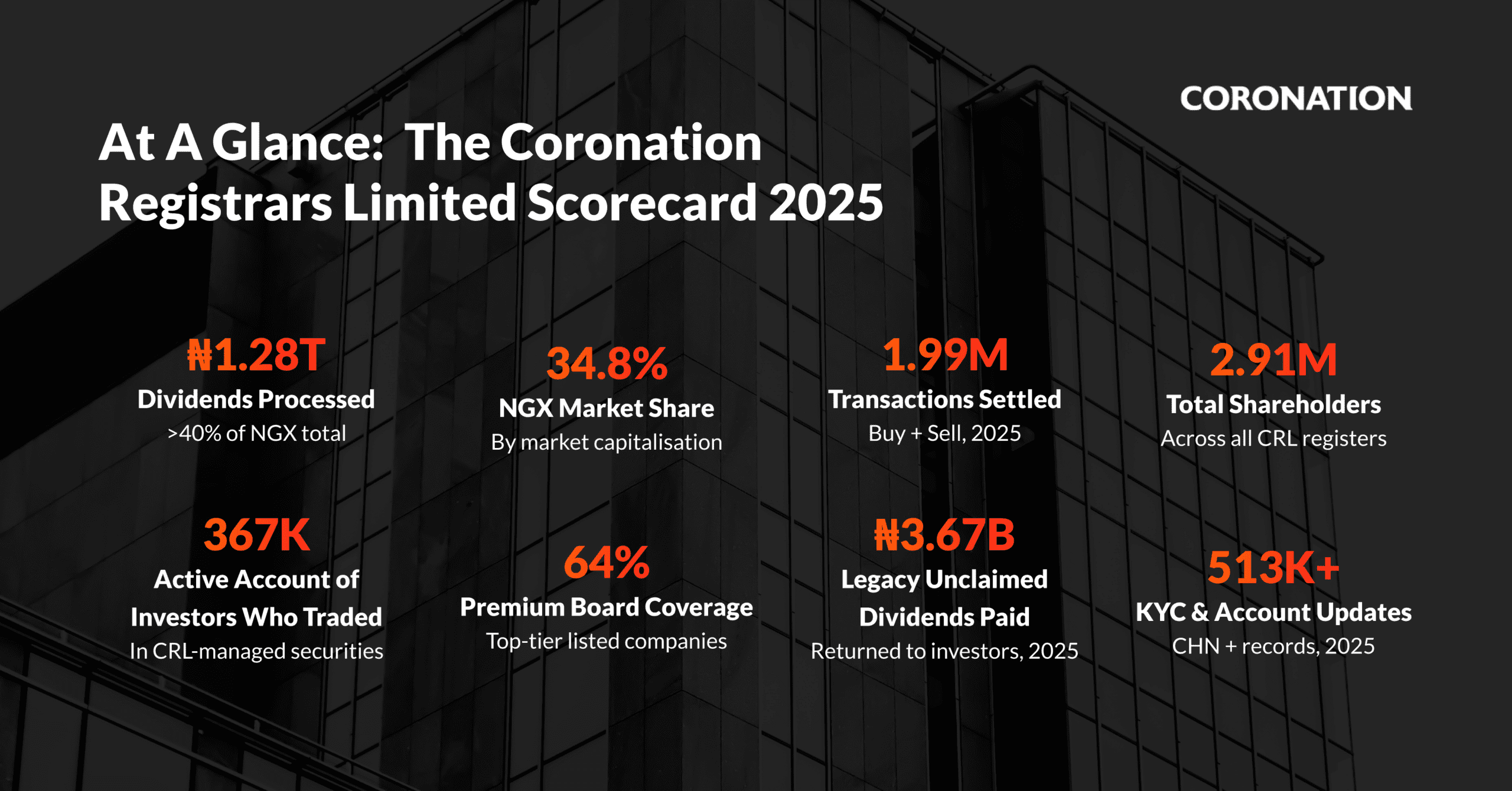

Coronation Registrars Processes ₦1.28 Trillion in Dividends, Records 34.8% NGX Market Share

Coronation Registrars Limited has released its 2025 performance scorecard, highlighting its continued role in supporting transparency, efficiency, and investor confidence Read more

Is Your Money Losing Value While Sitting in Your Bank Account?

For many people, saving money in a bank account feels like the safest financial decision. It gives you a sense Read more

Yield Watch 2026: Tracking Rate Movements and Lock-In Opportunities

In 2026, yields across Nigeria’s fixed-income market have drawn renewed attention from investors looking for steady income and capital preservation. Read more