What are Letters of Credit?

International trade often comes with challenges such as delayed payments and the risk of unfulfilled agreements. Letters of Credit offer a dependable solution. They act as a financial tool that bridges the gap between buyers and sellers across borders. These instruments simplify transactions while fostering trust in cross-border trading.

Letters of credit play an important role for businesses involved in importing or exporting. They facilitate smooth transactions and help address the risks associated with cross-border trade. Entrepreneurs can use this tool to expand their market reach while maintaining confidence in their business dealings.

This blog will explore the fundamentals of Letters of Credit, their types, and the step-by-step process involved. We will also discuss their benefits for businesses and highlight Coronation Merchant Bank’s trade finance solutions. This guide is designed to help you make informed decisions and grow your business through secure international transactions.

What is a Letter of Credit?

According to Article 1, UCP 600, a letter of credit is a commitment of the Issuing Bank (the bank serving the Buyer) to pay a certain amount of money within a certain period of time to the beneficiary (the seller), provided that the beneficiary presents a valid set of documents as specified in the Letter of Credit.

Put simply, it is a tool that makes buying and selling (imports and exports) across countries safer and easier. It is a promise from a bank to pay a seller on behalf of a buyer once certain conditions are met.

For example, if a business wants to buy goods from another country, the seller might worry about getting paid. The buyer’s bank can issue a Letter of Credit to reassure the seller. It guarantees payment once the seller proves they have shipped the goods.

This process protects both sides. The seller knows they will get their money after meeting the agreed terms, and the buyer knows they won’t pay until the goods are sent. Letters of Credit make trade smoother and help businesses build trust, even when they are far apart.

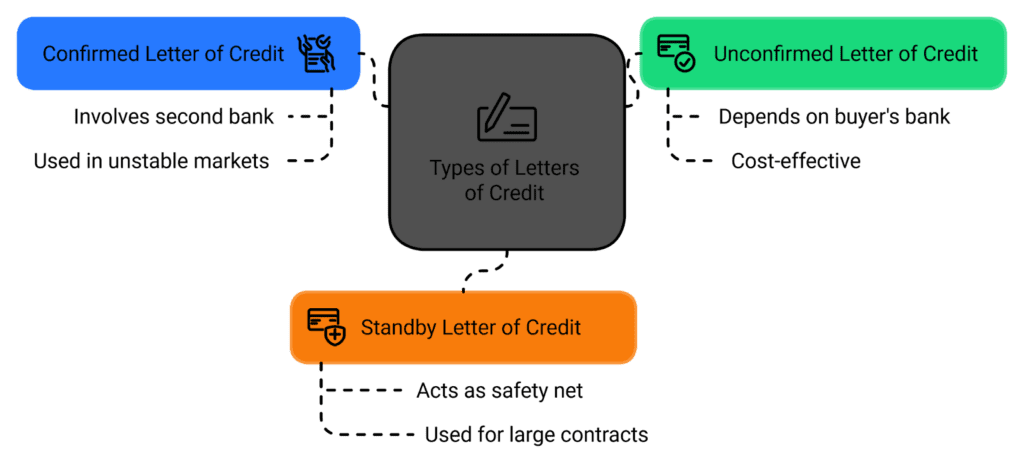

Types of Letters of Credit

Letters of Credit come in several types, each designed to support specific trade needs. These types offer different levels of security and flexibility depending on the nature of the transaction and the trust between the buyer and seller. Let’s break them down:

- Confirmed Letter of Credit

A confirmed Letter of Credit involves a second bank, usually in the seller’s country, that adds its own guarantee to pay the seller. This type is useful when the seller does not fully trust the buyer’s bank or when the trade involves countries with economic uncertainties. For example, a Nigerian exporter sending goods to a less stable market might request this type of extra assurance. - Unconfirmed Letter of Credit

In this case, only the buyer’s bank guarantees payment. It is simpler and may cost less than a confirmed Letter of Credit, but it also depends heavily on the buyer’s bank’s reliability. This type can be a straightforward option for sellers who trust the buyer’s bank. - Standby Letter of Credit

A standby Letter of Credit acts as a safety net. It is used when the buyer might face difficulties meeting their payment obligations. For instance, companies handling large contracts often use this to reassure their partners that payment will still be made even if issues arise.

These types of Letters of Credit help businesses handle different trade situations. The right choice depends on how much risk the buyer and seller are willing to take, the complexity of the transaction, and the level of trust between the parties involved.

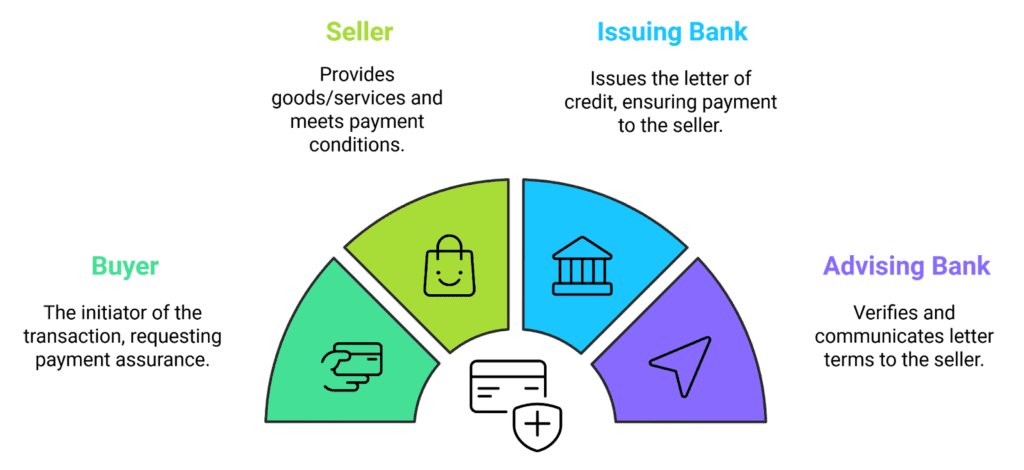

Key Parties Involved in Letters of Credit

Letters of credit involve several key players, each contributing to the smooth execution of trade transactions. Their combined roles help create a secure and structured process that reduces risks for all involved.

- Buyer

The buyer is the individual or company purchasing the goods or services. They request a letter of credit from their bank to assure the seller that payment will be made once all conditions are met. - Seller

The seller provides the goods or services and fulfils the conditions stated in the letter of credit. To receive payment, they must submit the required documents, such as shipping records or certificates of compliance, to their bank. - Issuing Bank

The issuing bank represents the buyer and takes responsibility for issuing the letter of credit. It guarantees that payment will be made to the seller if the specified conditions are satisfied. This bank is crucial in bridging the gap between buyers and sellers, especially in international transactions. - Advising Bank

The advising bank, often located in the seller’s region, acts as a messenger. It verifies the authenticity of the letter of credit and communicates its terms to the seller.

Each party plays an essential role in ensuring that letters of credit serve their purpose effectively. Through their collaboration, buyers and sellers can conduct transactions with greater confidence and reduced uncertainty.

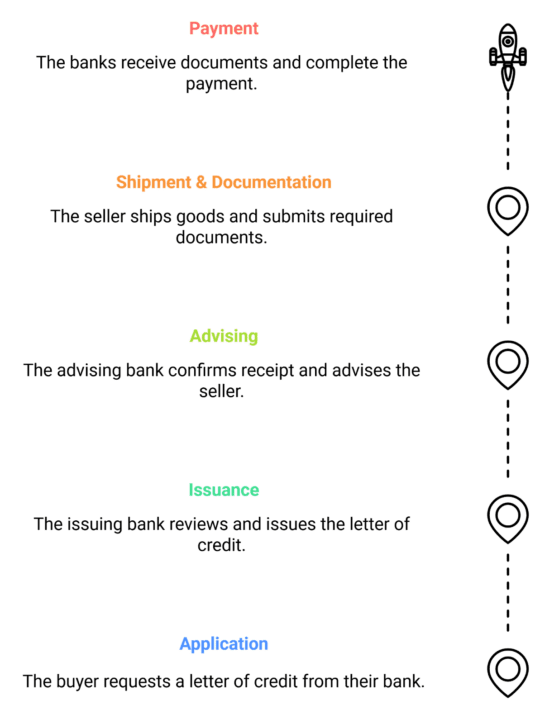

How Do Letters of Credit Work?

The process of using letters of credit involves several steps, each designed to protect both buyers and sellers during a transaction. This step-by-step explanation outlines how these financial instruments operate, especially in trade scenarios like importing or exporting goods.

- Application

The buyer begins the process by requesting a letter of credit from their bank. They provide details about the transaction, including the value of the goods, the seller’s information, and the terms for payment. For instance, an importer of electronics may apply for a letter of credit to assure their overseas supplier of secure payment. - Issuance

After reviewing the buyer’s application, the issuing bank agrees to proceed and issues the letter of credit. This document guarantees the seller will receive payment once they meet all the specified conditions. - Advising

The issuing bank forwards the letter of credit to an advising bank. The advising bank confirms receipt of the Letter of Credit and advises the seller accordingly. This step ensures the seller fully understands the requirements before shipping the goods. - Shipment and Documentation

The seller ships the goods as agreed and then submits the required documents to their bank, such as invoices, shipping details, and certificates. These documents prove that the conditions outlined in the letter of credit have been satisfied. - Verification and Payment

The advising bank reviews the submitted documents and forwards them to the issuing bank for final verification. If everything aligns with the terms of the letter of credit, the issuing bank releases the payment to the seller, completing the transaction.

This process creates a secure environment for trade, as letters of credit minimise risks for both buyers and sellers. They are especially beneficial in international transactions, providing assurance to all parties and fostering trust in cross-border trade.

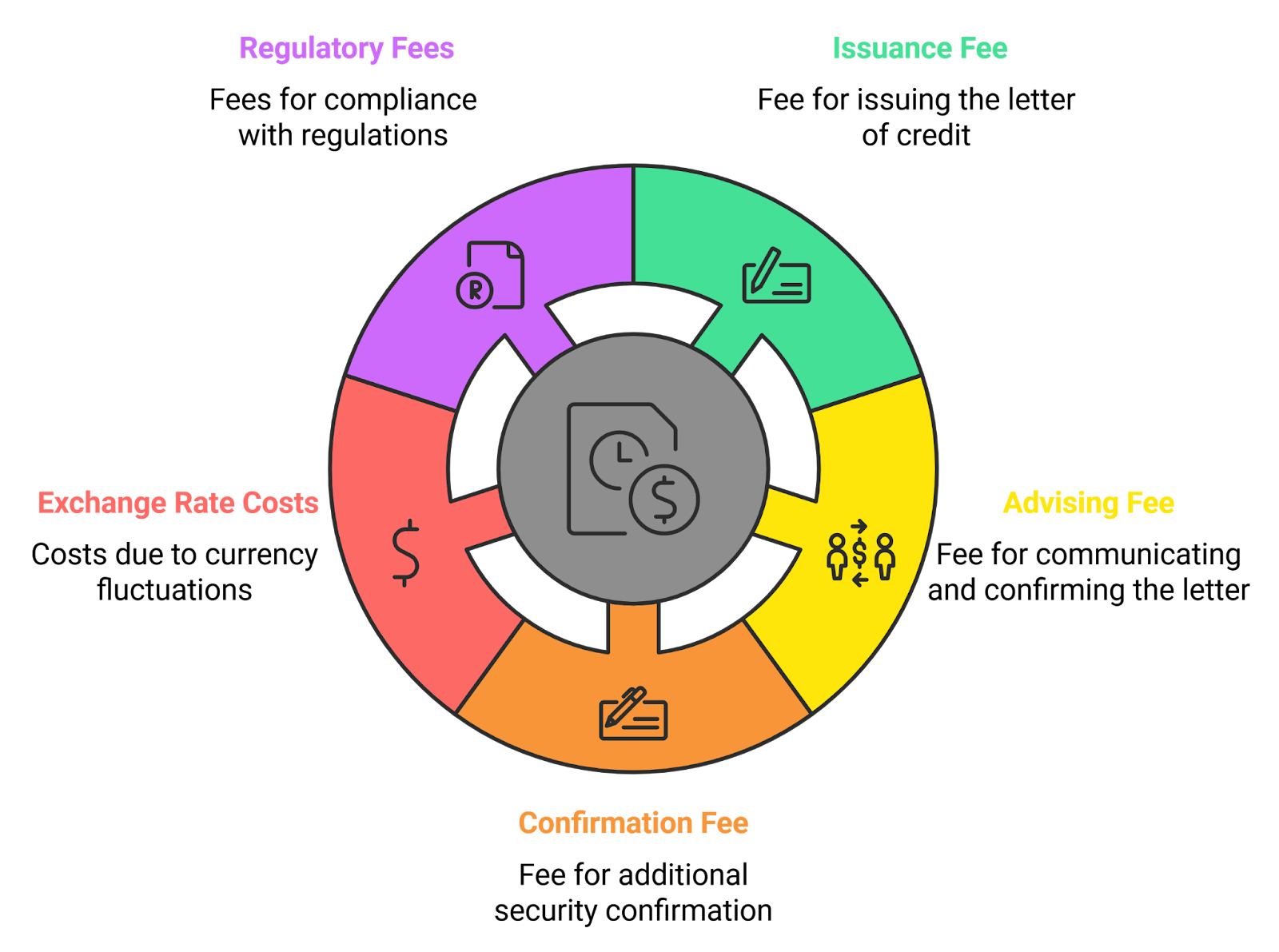

Letters of Credit Fees and Costs

When using letters of credit, businesses should be aware of the various fees and costs involved. These charges can vary depending on the banks, the nature of the transaction, and the specific requirements of the agreement. Here are a few of the most common costs.

- Issuance Fee: Banks charge a percentage of the total transaction value for issuing the letter of credit. This fee compensates the issuing bank for guaranteeing payment to the seller.

- Advising Fee: The advising bank charges a fee to communicate the letter of credit to the seller.

- Confirmation Fee: If the seller requests confirmation from another bank to add extra security, this service incurs a separate fee.

- Exchange Rate Costs: For Nigerian businesses, additional costs may arise due to exchange rate fluctuations, especially when dealing with foreign currencies.

- Regulatory and Compliance Fees: Banks may apply fees in line with Central Bank of Nigeria (CBN) regulations for international trade transactions.

Frequently Asked Questions

What documents are required for Letters of Credit (LC)?

The specific documents required for a letter of credit depend on the terms agreed upon by the buyer and seller. Commonly requested documents include:

- Commercial Invoice: Details the goods sold, quantities, and agreed price.

- Bill of Lading or Airway Bill: Confirms shipment.

- Packing List: Lists the items, quantities, and packaging details.

- Certificate of Origin: Indicates where the goods were manufactured.

- Insurance Certificate: Ensures the goods are covered against potential risks during transport.

- Inspection Certificate: Verifies the quality and quantity of goods, usually issued by an inspection agency.

The issuing bank will specify any additional documents required based on the agreement.

Who pays for a Letter of Credit?

The buyer, also known as the applicant, typically bears the cost of a letter of credit. This includes issuance fees, advising fees, confirmation fees (if applicable), and other bank charges. However, in some cases, the seller and buyer may agree to share these costs. The terms of cost-sharing are usually outlined in the trade agreement.

How long is an LC valid for?

A letter of credit’s validity period depends on the terms negotiated between the buyer and seller. Typically, it is valid until the shipment and payment obligations are fulfilled. Standard durations are 60 to 90 days, but it can be longer for complex or high-value transactions. The expiration date is explicitly stated in the LC, and all required actions, such as shipment and document submission, must be completed before this date.

What is the difference between a bank guarantee and a Letter of Credit?

- Purpose: A letter of credit guarantees payment to the seller if the terms are met, acting as a payment mechanism. A bank guarantee provides compensation if one party fails to fulfill contractual obligations, offering protection for the other party.

- Trigger for Payment: In an LC, payment is made upon submission of required documents. In a bank guarantee, payment is made only if the applicant defaults.

- Risk Coverage: An LC reduces payment risk in trade transactions, while a bank guarantee covers performance or contractual risks.

- Usage: LCs are commonly used in international trade, while bank guarantees are used in broader financial transactions, such as construction or real estate deals.

What happens if a letter of credit is not paid?

If a letter of credit is not paid, several scenarios may arise:

- Legal Disputes: If the issuing bank fails to pay despite proper compliance, the beneficiary (seller) may seek legal remedies or rely on any additional confirmation bank for payment.

Is an LC transferrable?

Not all letters of credit are transferable. Only a transferable LC, explicitly marked as such, allows the original beneficiary (seller) to transfer part or all of the credit to a second beneficiary. This feature is commonly used in transactions involving intermediaries or traders. Non-transferable LCs cannot be reassigned, and payment is made exclusively to the named beneficiary.

Conclusion

Letters of credit offer significant benefits to businesses involved in international trade. They provide security for both buyers and sellers, guarantee payments, and help build trust in cross-border transactions. Coronation Merchant Bank offers bespoke solutions that meet the unique needs of businesses. With expertise in trade finance and a deep understanding of the challenges in global markets, we ensure smooth, reliable transactions.

If you’re looking to expand your business through international trade, contact Coronation Merchant Bank today for a reliable and trusted partner in letters of credit and trade finance solutions.

Contact us:

Website: www.coronationmb.com

Email: crc@coronationmb.com

Phone: +234 (0)2-0188 87640

Related Posts

What Smart Investors Do When Interest Rates Start Falling

When interest rates start falling, the biggest opportunities are often already in motion. Yet many investors make the same mistake; Read more

The Biggest Investment Mistake Nigerians Make During Economic Uncertainty

For most young professionals in Nigeria, income feels predictable. Salary comes in, expenses go out, and whatever is left is Read more

What Happens When Income Stops? Retirement Planning Redefined

For most people, income feels predictable.It comes in regularly. It supports everything, from daily expenses to long-term plans. Over time, Read more

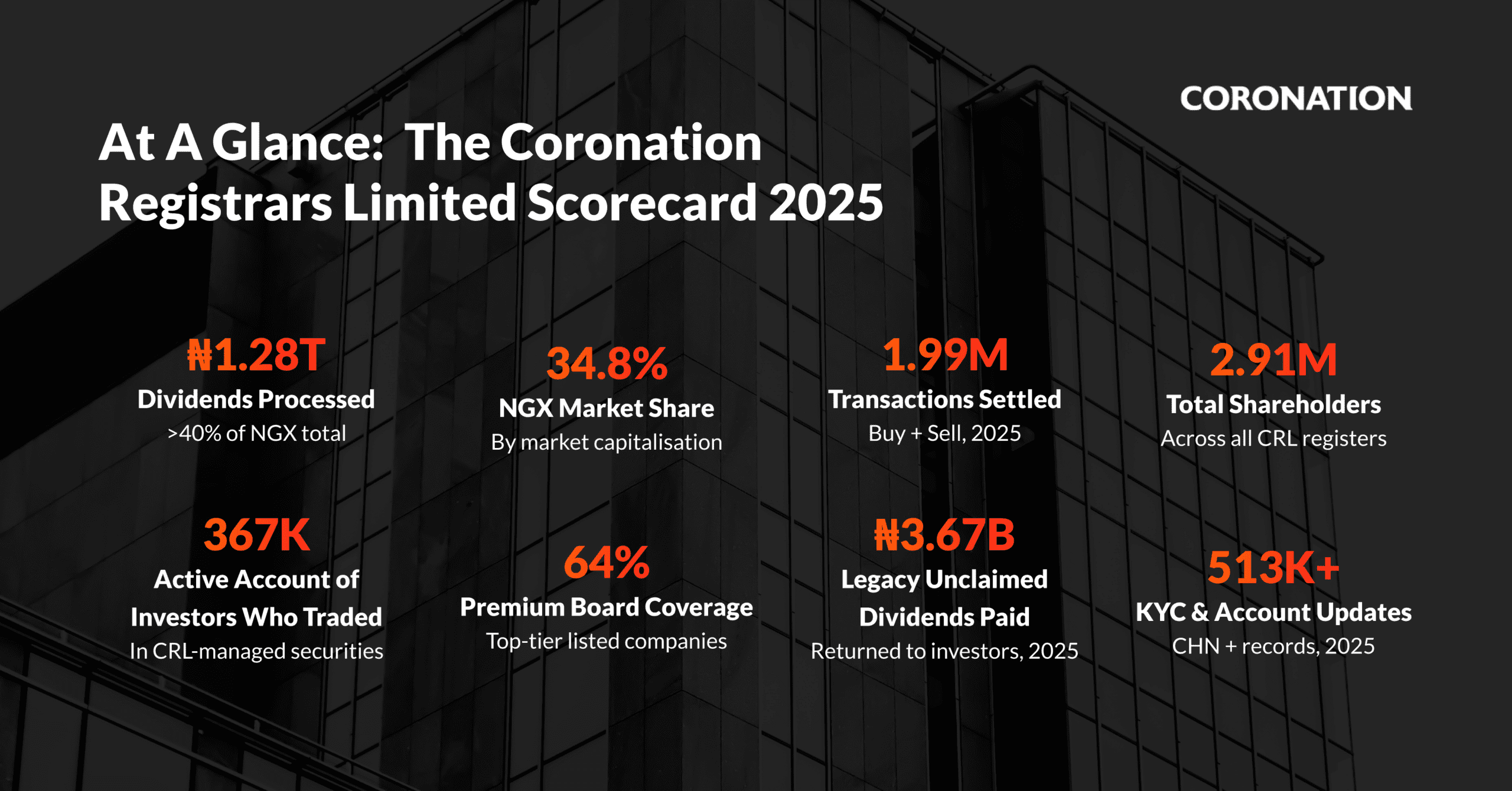

Coronation Registrars Processes ₦1.28 Trillion in Dividends, Records 34.8% NGX Market Share

Coronation Registrars Limited has released its 2025 performance scorecard, highlighting its continued role in supporting transparency, efficiency, and investor confidence Read more