The Nigerian economy faces a dual challenge: the drastic depreciation of the Naira and soaring inflation rates. But first, what is driving the fall of the naira?

The Nigerian Naira (NGN) has experienced significant depreciation against major currencies. As the exchange rate fluctuates, the purchasing power of the Naira diminishes.

The Nigerian economy, like many others, grapples with the ebb and flow of foreign exchange (FX) rates, particularly the fluctuating value of the naira against the dollar. Recent times have witnessed heightened volatility in these rates, prompting concerns among investors and businesses alike. Understanding the underlying drivers behind the fall of the naira and exploring strategies to shield one’s portfolio from its impacts are crucial endeavours in today’s economic landscape.

Factors driving the fall of the naira:

The depreciation of the naira is propelled by a confluence of factors, each exerting its influence on the FX market dynamics. Chief among these is the substantial reliance on imports across various sectors of the economy. Even seemingly trivial products, along with essential commodities like agro-products that we also have here, contribute to the demand for foreign currency, placing downward pressure on the naira.

Additionally, the scarcity of dollars, heightened by challenges in repatriating funds, further exacerbates the depreciation spiral.

Government interventions and policy measures:

In response to the escalating FX volatility, the Nigerian government and the Central Bank of Nigeria (CBN) have embarked on a series of interventions and policy measures aimed at stabilising the currency market.

The decision to float the naira, coupled with a comprehensive strategy to enhance liquidity in the forex market, reflects concerted efforts to address the root causes of the currency depreciation.

These initiatives include unifying FX market segments, clearing outstanding FX obligations, and introducing new operational mechanisms for Bureau De Change operators. Also, stringent measures such as enforcing the Net Open Position limit for commercial banks and adjusting the remunerable Standing Deposit Facility Cap underscore the resolve to restore stability to the FX market.

Insights from the Central Bank:

The Central Bank of Nigeria (CBN) has provided insights into the factors driving the depreciation of the naira, shedding light on the magnitude of foreign exchange expenditure by Nigerians.

According to the CBN, expenditures on foreign trips, medical tourism, and overseas education amounted to a staggering $98 billion. This figure surpasses the total foreign exchange reserves held by the apex bank, underscoring the magnitude of the challenge driven by capital flight and foreign currency demand.

The inflation challenge

Inflation rates have surged (29.9% as of January 2024), eroding the real value of money. When prices rise faster than your savings can keep up, your wealth effectively shrinks. The cost of living increases, affecting everything from garri to housing.

To arrest the rising inflation, the Monetary Policy Committee of the CBN increased the benchmark interest rate by 400 basis points to a record 22.75%.

How can you protect your portfolio amidst FX volatility?

Navigating the volatile FX landscape requires a strategic approach to portfolio management.

i. Currency diversification:

Diversifying your portfolio across multiple currencies can serve as a hedge against currency risk. Allocating a portion of your assets to stable currencies or those exhibiting less volatility can help mitigate the impact of adverse FX movements on your overall portfolio value.

In order words, consider opening accounts denominated in stable foreign currencies (e.g., USD, EUR, GBP). These accounts act as a buffer against Naira fluctuations. Also, while volatile, cryptocurrencies like Bitcoin offer an alternative store of value, research thoroughly and invest cautiously.

ii. Use of derivatives:

Leveraging derivatives such as forward contracts and currency options can provide protection against adverse FX movements. These financial instruments allow investors lock in exchange rates for future transactions, thereby reducing exposure to currency risk.

iii. Invest in non-currency assets:

Consider allocating a portion of your portfolio to non-currency assets such as real estate, commodities, or equities. These assets may exhibit a lower correlation with currency movements, offering diversification benefits and reducing overall portfolio risk.

Gold and silver historically retain value during economic uncertainties. Consider allocating a portion of your savings to these metals.

iv. Fixed-Income Investments:

a. Treasury Bills and Bonds

These government-backed instruments offer fixed returns. While not immune to inflation, they provide stability.

Consider short-term and long-term options.

b. Inflation-linked bonds

These bonds adjust interest rates based on inflation. Your returns keep pace with rising prices.

Consult with financial advisors to choose suitable bonds.

v. Stock market participation:

a. Equities

Invest in well-researched stocks. Companies with strong fundamentals can outperform inflation.

Diversify across sectors to spread risk.

b. Diversified mutual funds

These funds pool money from multiple investors and invest in various assets (stocks, bonds, real estate).

Professional fund managers handle the portfolio.

vi. Risk Management:

a. Emergency fund

Maintain a liquid emergency fund (3-6 months’ worth of expenses) to cover unforeseen events.

An emergency fund prevents you from dipping into long-term investments during crises.

b. Debt management

Avoid high-interest debt. Pay off existing debts promptly. High debt burdens compound financial stress.

vii. Stay informed and flexible:

Keeping abreast of economic indicators, geopolitical developments, and central bank policies can help you as an investor anticipate FX market movements and adjust their portfolios accordingly. Maintaining flexibility in investment decisions allows for timely adjustments in response to changing market conditions.

viii. Consult a financial advisor:

Seek professional advice tailored to your specific circumstances. A financial advisor can guide you through personalised strategies based on your risk tolerance, investment horizon, and financial goals. At Coronation, our expert financial advisors can provide you tailored plan to suit your financial goals. Contact a financial advisor here.

Remember, no strategy is fool proof. Adapt your approach as needed and stay vigilant. By proactively hedging, you can protect your savings and weather the economic challenges effectively.

Disclaimer: This article provides general information and does not constitute financial advice. Consult a professional before making any financial decisions.

Related Posts

What Smart Investors Do When Interest Rates Start Falling

When interest rates start falling, the biggest opportunities are often already in motion. Yet many investors make the same mistake; Read more

The Biggest Investment Mistake Nigerians Make During Economic Uncertainty

For most young professionals in Nigeria, income feels predictable. Salary comes in, expenses go out, and whatever is left is Read more

What Happens When Income Stops? Retirement Planning Redefined

For most people, income feels predictable.It comes in regularly. It supports everything, from daily expenses to long-term plans. Over time, Read more

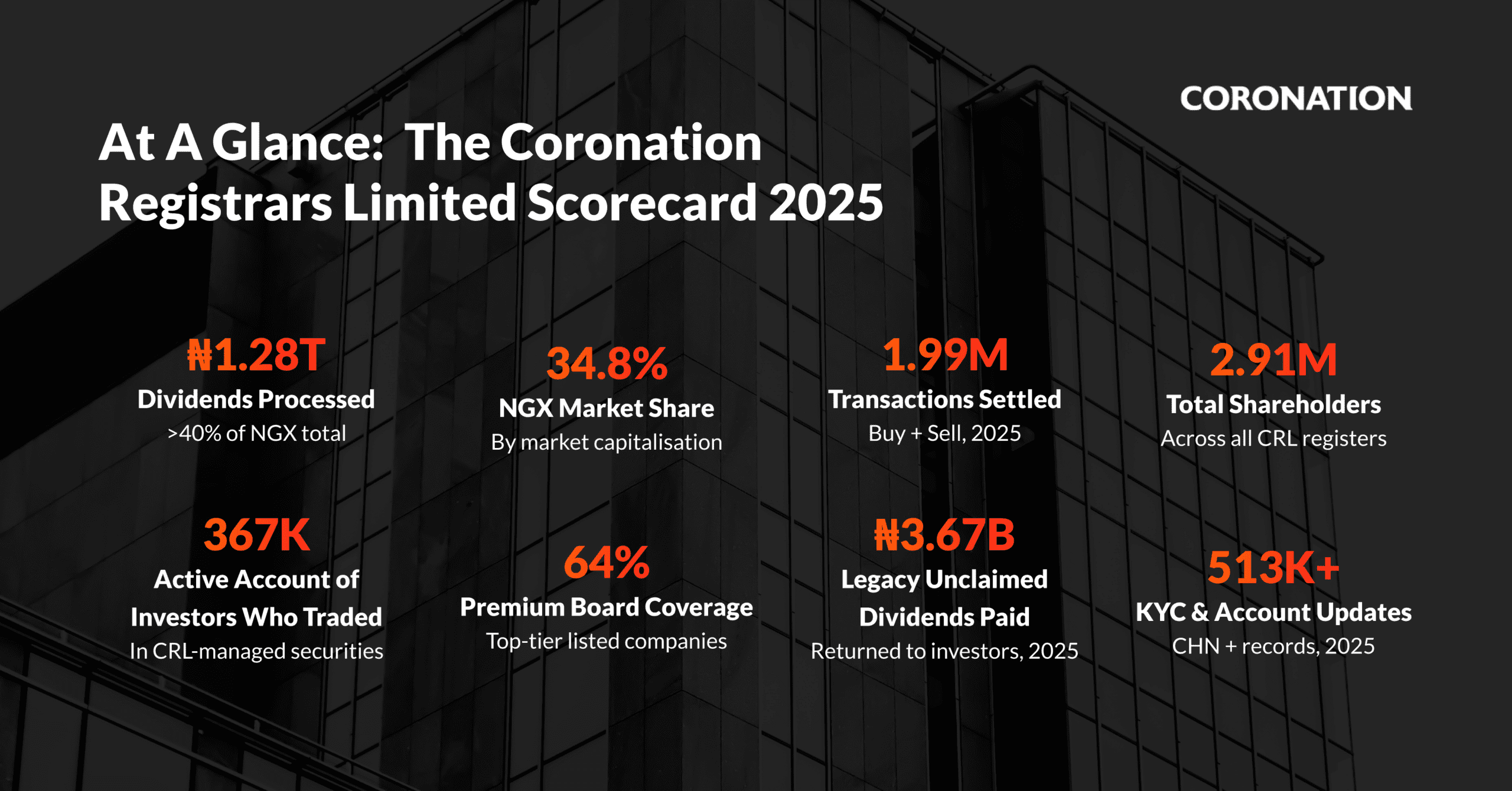

Coronation Registrars Processes ₦1.28 Trillion in Dividends, Records 34.8% NGX Market Share

Coronation Registrars Limited has released its 2025 performance scorecard, highlighting its continued role in supporting transparency, efficiency, and investor confidence Read more